A defender-framed guide for fintech and bank security leaders: what makes a money-moving agent's attack surface unique, the transaction-authorization abuse classes to scope, what a clean result looks like, and the controls to demand.

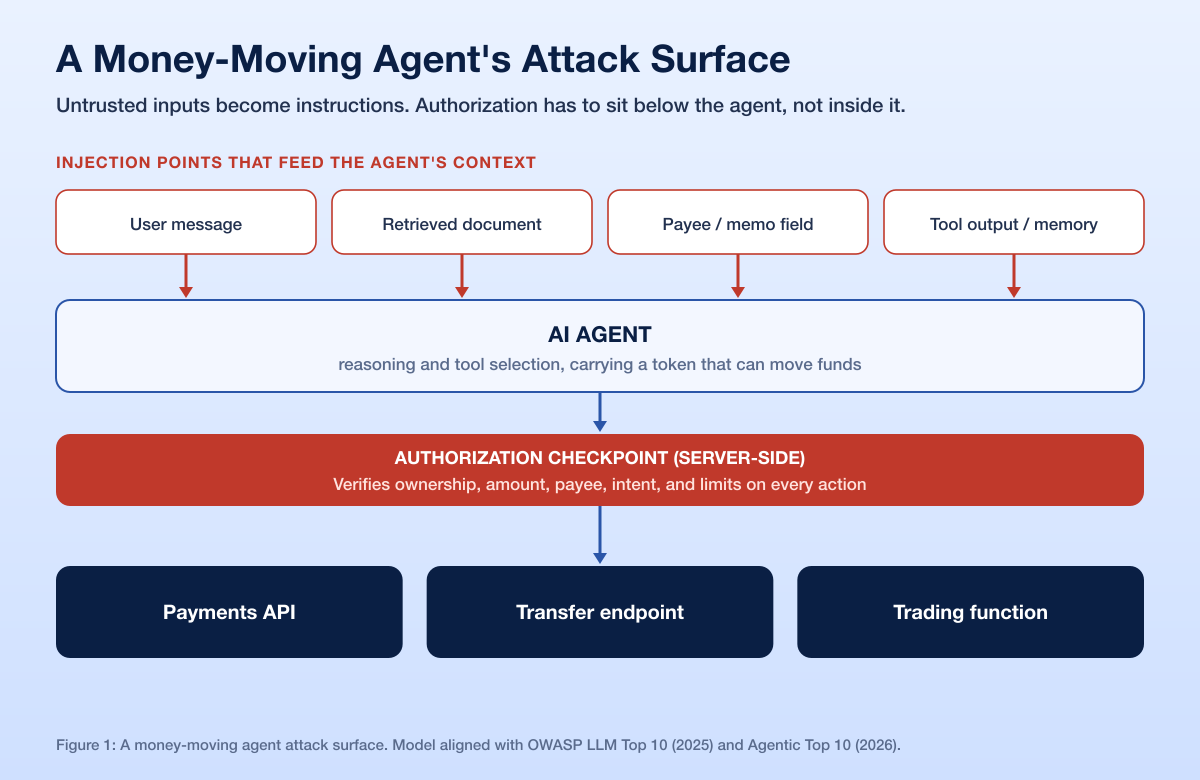

Gartner forecasts that AI agents will intermediate more than US$15 trillion in B2B spending by 2028 (Gartner, via Digital Commerce 360). Fintech is wiring language models straight to the ledger: assistants that pay invoices, move balances, and place trades. The moment an agent can call a payments API, its failures stop being awkward chatbot transcripts and become unauthorized transfers.

So how do you red team an AI agent that can move money, and what is unique about its attack surface? You scope the whole engagement to one question: can an attacker cause the agent to authorize a financial action the user never intended, using only the inputs the agent is designed to accept? The unique surface is the seam where the agent's reasoning meets the money-moving tools it can call. Text that looks like a normal request, a payee note, or a retrieved document becomes an instruction, and the instruction becomes a transfer. That is fintech AI red teaming: transaction-authorization abuse as the objective, not a footnote.

This post assumes the general agentic taxonomy and prompt-injection basics, which Stingrai covers in its field guide to AI red teaming for LLM and agentic apps. Here we stay on the money-moving core: the five threat classes to scope, how to draw the boundary, and the controls a bank or fintech should demand. The regulatory anchor is PCI DSS 4.0.1, which already treats an autonomous agent as an actor that needs its own identity and audit log.

TL;DR: Red Teaming a Money-Moving AI Agent

The blast radius is money, not data (2028): Gartner forecasts AI agents will intermediate more than US$15 trillion in B2B spending by 2028 (Gartner, via Digital Commerce 360).

The core test is transaction-authorization abuse: whether the agent can be driven to authorize a payment, transfer, or trade the user never approved.

Prompt injection is the delivery mechanism (2025): it holds LLM01 in the OWASP Top 10 for LLM Applications 2025; it is how a hostile instruction reaches a money-moving tool.

Goal hijack and tool misuse are named agent risks (2026): ASI01 and ASI02 lead the OWASP Top 10 for Agentic Applications 2026, published December 9, 2025.

PCI DSS 4.0.1 already governs the agent (2024): each actor in the cardholder data environment needs a unique identity (Requirement 8) and all access must be logged (Requirement 10) (PCI SSC).

Scope is the whole battle: an application-layer agent test is narrower and sharper than a full DORA threat-led penetration test, and the two should not be confused.

Key Takeaways

The money-moving action is the entire test. A model that says something impolite is a content problem; a model that signs a transfer is a security incident. Fintech AI red teaming succeeds or fails on one question: can the agent be induced to authorize money movement outside the user's intent?

Prompt injection is not the vulnerability. The unguarded transfer is. Injection is how a hostile instruction arrives (LLM01 in the OWASP LLM Top 10). The exploitable flaw is an authorization decision the agent is trusted to make in natural language.

Authorization must live below the agent, not inside it. If the only thing between a crafted input and a wire is the model's judgment, the model is your access-control layer, and models are steerable. A clean result puts the payments service, not the agent, in charge of limits, approvals, and ownership.

This is an application-layer test, distinct from a DORA threat-led pentest. A money-moving agent assessment is scoped to one application and its money-moving tools; a DORA threat-led test is an intelligence-led exercise against a financial entity's critical live functions. Buy the right one for the question you are asking.

Sources and Scope

This guide draws on primary publications verified with a research cutoff of July 7, 2026: the OWASP Top 10 for LLM Applications 2025 and Top 10 for Agentic Applications 2026 for risk-class names, PCI DSS v4.0.1 for identity and logging, the NIST AI Risk Management Framework for governance, and Gartner for scale. Every attack description below is synthetic and defender-oriented: it describes what to test and what a clean result looks like, with no working payloads or attacker instructions.

What Makes a Money-Moving Agent's Attack Surface Unique

A read-only assistant that summarizes a statement has a data-exposure problem. A money-moving assistant has an action problem, and the difference reshapes the whole engagement.

The unique surface is the point where the agent's reasoning meets a tool that changes a balance. The customer talks to an agent, the agent decides what to do, and the agent calls tools: a payments API, a transfer endpoint, a trading function. Every input in the agent's context is a potential instruction: the user's message, a retrieved document, a payee name, a memo field, a prior-turn memory. Any of them can carry text the model treats as a command, and when that command reaches a money-moving tool the model has become an unauthorized signer.

Three properties make this harder than a classic web test. The boundary is semantic, not syntactic: no special character marks "this is data, not an instruction," so the agent can be talked into what a parser never would. Agents chain steps, so a benign action early in a session can set up a harmful one later. And the agent usually carries real authority, holding a token that can already move funds, so a successful manipulation inherits that authority immediately. The data that feeds the agent is part of this surface too, which is why poisoned context is closely related to RAG and vector-store access-control testing.

The Five Money-Moving Threat Classes to Test

Scope five classes explicitly. For each, the useful artifact is a pair: what to test, and what a clean result looks like.

1. Transaction-authorization abuse

The core class and the reason the engagement exists. The tester probes whether the agent will authorize a payment, transfer, or trade the account owner did not approve: to a payee the user never named, above the amount the user agreed, or on an account the user does not own.

What to test: whether the payments service checks ownership, amount, payee, and intent on every action, independent of what the agent asserts. Clean result: the service independently verifies account ownership, applies the same payee controls a human would, and enforces a server-side limit. The agent's say-so is never sufficient.

2. Goal hijacking into a transfer

Goal hijack is ASI01 in the OWASP Agentic Top 10. The tester checks whether content the agent ingests, a support ticket, an uploaded invoice, a retrieved help article, can redirect the agent from what the user asked toward moving funds.

What to test: whether any non-user input can escalate a read-only intent into a money-moving action without fresh, explicit user authorization. Clean result: ingested content can inform an answer but can never initiate or approve a transfer on its own; money movement requires a distinct confirmation tied to the authenticated user.

3. Tool-misuse chains

Tool misuse is ASI02 in the OWASP Agentic Top 10. Agents compose actions, so the tester looks for chains where individually reasonable tool calls combine into an unauthorized outcome: read a payee, create a payee, fund the payee, all steered by manipulated intermediate output.

What to test: whether the payments service reasons about the whole sequence rather than each isolated call, and whether limits apply to the chain. Clean result: adding a payee and sending money are governed by controls that see the sequence, with velocity limits, cooling-off on new payees, and step-up authentication a chain cannot skip.

4. Advice manipulation

Not every money-moving agent presses the button; some influence a human who does. The tester checks whether the agent can be steered to give financially harmful guidance: nudging a user toward a fraudulent payee, downplaying a scam warning, or recommending a transfer that benefits an attacker.

What to test: whether hostile input can bias the agent's advice on payments, recipients, or risk. Clean result: fraud checks, payee-risk warnings, and scam interdiction fire from services outside the agent, so a manipulated recommendation still meets the same guardrails a user would see without it.

5. Over-broad agent permissions

The cheapest finding to prevent is excessive agency, LLM06 in the OWASP LLM Top 10. The tester inventories what the agent's identity is actually allowed to do: which tools, which accounts, which ceilings. An agent holding a broad payments scope it rarely needs is a standing liability regardless of any specific exploit.

What to test: whether the agent's credentials are least-privilege, scoped to the minimum tools and amounts for its job, and whether a single compromise is bounded. Clean result: the agent runs with narrowly scoped, short-lived credentials, per-action and per-day ceilings, and no access to functions outside its stated purpose.

Drawing the Scope: What Is In, What Is Out

The money-moving core is always in scope: the agent's decision loop, the tools that change balances, the authorization and logging around those tools, and the data sources that feed the agent's context. Prompt injection, goal hijack, and tool misuse are tested as means to that end, not as a general model-safety survey.

Two clarifications keep the engagement honest. Testing the agent's behavior is different from testing the application it runs on. The banking web app and its APIs still need a rigorous web application penetration test for IDOR, broken authorization, and business-logic flaws, because those are frequently the mechanism a manipulated agent exploits: an authorization check the app fails to enforce is a hole whether a human or an agent walks through it. And this test is not a substitute for a DORA threat-led penetration test, an intelligence-led exercise against a financial entity's critical live functions. A money-moving agent assessment is one focused input to that broader program, not a replacement.

The division of labor is straightforward. Autonomous tooling is strong at the deterministic application layer, where Stingrai's Snipe hunts IDOR, business-logic, and broken-authorization flaws across the banking web app and API. Senior human pentesters drive the adversarial agent-behavior work: the goal-hijack attempts, tool-misuse chains, and transaction-authorization probes that require creativity. For a pre-launch assistant, the same discipline scales into a pre-launch chatbot red-team checklist.

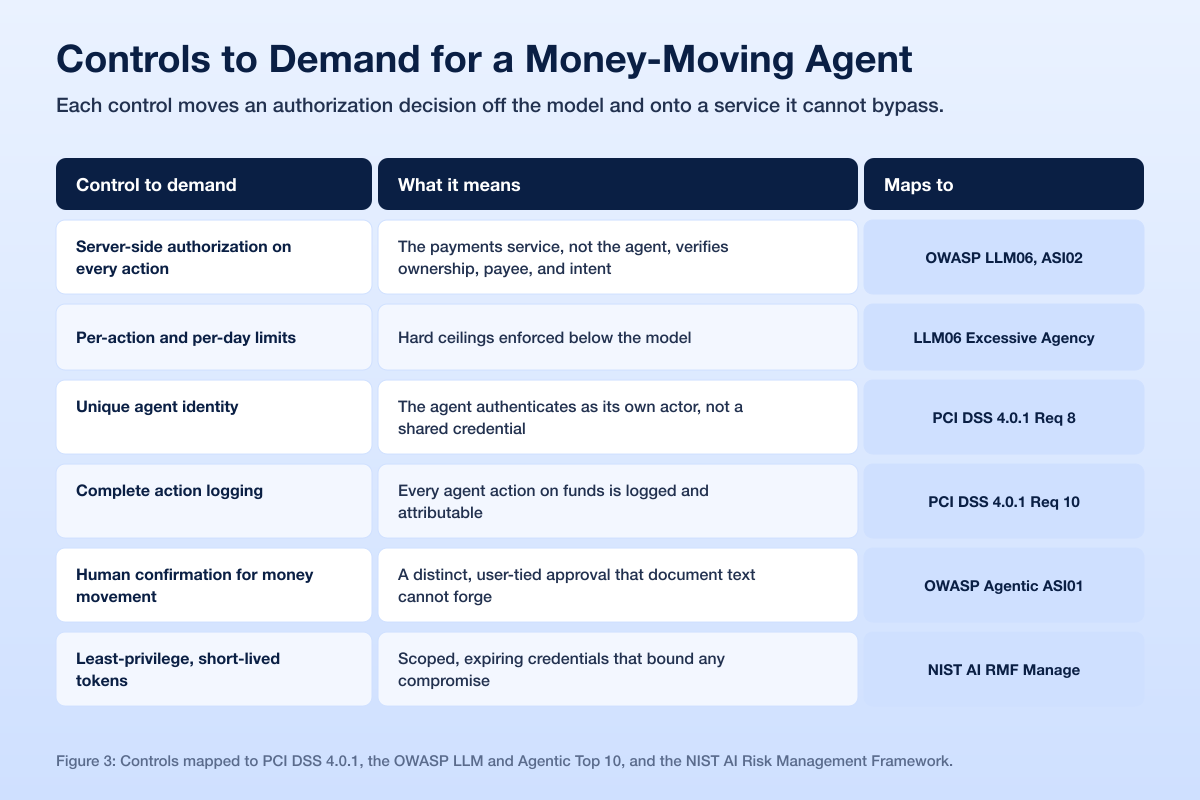

Controls to Demand, Mapped to PCI DSS 4.0.1, OWASP, and NIST

The strongest outcome of a money-moving agent test is confirmation that the controls below hold, because they move authorization off the model and onto services the model cannot talk its way past.

Control to demand | What it means | Maps to |

|---|---|---|

Server-side authorization on every action | The payments service, not the agent, verifies ownership, payee, and intent | OWASP LLM06, Agentic ASI02 |

Per-action and per-day limits | Hard ceilings enforced below the model | OWASP LLM06 Excessive Agency |

Unique agent identity | The agent authenticates as its own actor, not a shared credential | PCI DSS 4.0.1 Requirement 8 |

Complete action logging | Every agent action on funds is logged and attributable | PCI DSS 4.0.1 Requirement 10 |

Human confirmation for money movement | A distinct, user-tied approval that document text cannot forge | OWASP Agentic ASI01 Goal Hijack |

Least-privilege, short-lived tokens | Scoped, expiring credentials that bound any compromise | NIST AI RMF Manage function |

The regulatory hook is worth stating plainly. PCI DSS 4.0.1, published by the PCI Security Standards Council on June 11, 2024, does not mention AI agents, but its existing rules already reach them (PCI SSC). An autonomous agent acting in the cardholder data environment is an actor: Requirement 8 says every actor needs a unique identity, so the agent should not borrow a human's credentials, and Requirement 10 says all access must be logged, so every action it takes on money must be attributable. If you cannot answer "which agent identity did this, and where is the log," you have a gap that predates any exploit. The NIST AI Risk Management Framework and its Generative AI Profile wrap these controls in a Govern, Map, Measure, Manage lifecycle so the testing is a program, not a one-off.

What This Means for Fintech Security Leaders

Scope the engagement to money movement. Treat transaction-authorization abuse as the objective, with goal hijack, tool misuse, advice manipulation, and excessive agency as the routes to it. A generic model-safety report will not tell you whether your ledger is reachable.

Move authorization below the agent before you test. Every limit, ownership check, and approval that lives in a service rather than the model is a finding you will never have to receive.

Give the agent its own identity and log everything it does. This is a PCI DSS 4.0.1 expectation, and the difference between a contained incident and an unbounded one.

Pentest the underlying app, not just the agent. A manipulated agent usually exploits a real application flaw, so keep a rigorous web and API pentest in the program.

Run it continuously. Every new tool, prompt change, or model swap can reopen the authorization surface, which is why continuous PTaaS fits money-moving agents better than an annual check.

Stingrai runs this work as a hybrid. Snipe, Stingrai's autonomous web-application penetration testing agent, drives the application layer of the banking web app and API: it is purpose-built to hunt IDOR, business-logic, and broken-authorization flaws, generates AutoFix pull requests, and can run as a PR-gating check. Senior human pentesters lead the adversarial agent-behavior testing that decides whether the agent can be turned into an unauthorized signer. The evidence supports your PCI DSS 4.0.1 and SOC 2 programs, and Stingrai is a CREST-accredited penetration testing provider headquartered in Toronto with a London office. Explore the red teaming and PTaaS pages, or see current packages on the pricing page.

Frequently Asked Questions

How do you red team an AI agent that can move money, and what is unique about its attack surface? You scope the entire engagement to one question: can an attacker cause the agent to authorize a payment, transfer, or trade the user never intended, using only the inputs the agent is designed to accept? The unique surface is the seam where the agent's reasoning meets a money-moving tool. Because the boundary between data and instruction is semantic rather than syntactic, ordinary-looking text in a message, document, payee note, or memory can become a command that reaches the ledger. Testing focuses on transaction-authorization abuse, goal hijack, tool misuse, advice manipulation, and excessive agency.

What is transaction-authorization abuse testing? It is the core of a money-moving agent engagement: probing whether the agent can be steered into authorizing a financial action outside the user's intent, to an unapproved payee, in an excessive amount, or on an account the user does not own. A clean result is that the payments service independently verifies ownership, payee, amount, and intent on every action, so the agent's assertion alone can never move funds.

Is prompt injection the main risk for a money-moving agent? Prompt injection is the delivery mechanism, not the underlying vulnerability. It holds LLM01 in the OWASP Top 10 for LLM Applications 2025 and is how a hostile instruction reaches a tool. The exploitable flaw is an authorization decision the agent is trusted to make. When limits, approvals, and ownership checks are enforced by services below the model, a successful injection has nothing to act on.

Does PCI DSS 4.0.1 apply to AI agents? PCI DSS 4.0.1 does not name AI agents, but its requirements reach any actor in the cardholder data environment. Requirement 8 means the agent needs a unique identity rather than a shared or borrowed credential, and Requirement 10 means every action it takes on funds must be logged and attributable (PCI SSC).

Can Stingrai test our fintech AI agent? Yes. Stingrai runs a hybrid engagement: Snipe, its autonomous web-application agent, tests the banking web app and API for IDOR, business-logic, and broken-authorization flaws, while senior human pentesters drive the adversarial agent-behavior testing for transaction-authorization abuse, goal hijack, and tool misuse. The work supports your PCI DSS 4.0.1 and SOC 2 evidence. Start on the PTaaS or red teaming pages.

References

Gartner (reported by Digital Commerce 360). Gartner: AI agents will command $15 trillion in B2B purchases by 2028. November 28, 2025. https://www.digitalcommerce360.com/2025/11/28/gartner-ai-agents-15-trillion-in-b2b-purchases-by-2028/. Forecasts AI agents intermediating more than US$15 trillion in B2B spending by 2028 and 20 percent of monetary transactions programmable by 2030.

OWASP GenAI Security Project. OWASP Top 10 for LLM Applications 2025. https://genai.owasp.org/llm-top-10/. Source of LLM01 Prompt Injection and LLM06 Excessive Agency.

OWASP GenAI Security Project. OWASP Top 10 for Agentic Applications 2026. Published December 9, 2025. https://genai.owasp.org/resource/owasp-top-10-for-agentic-applications-for-2026/. Source of ASI01 Agent Goal Hijack and ASI02 Tool Misuse and Exploitation.

PCI Security Standards Council. Just Published: PCI DSS v4.0.1. June 11, 2024. https://blog.pcisecuritystandards.org/just-published-pci-dss-v4-0-1. Confirms the limited revision and the identity (Requirement 8) and logging (Requirement 10) obligations for actors in the cardholder data environment.

NIST. AI Risk Management Framework and Generative AI Profile. https://www.nist.gov/itl/ai-risk-management-framework. Govern, Map, Measure, and Manage functions for AI system risk.